Adjusting Entries When Refunds & Credit Notes Flow Mid-Cycle

The core purpose of adjusting entries is to accurately match revenue and expenses to the periods in which they were earned or incurred, aligning financials with the economic reality of operations. Without them, P&Ls distort business performance, revenue schedules break, and audit-readiness becomes a scramble.

At scale, however, these entries aren’t just periodic—they’re dynamic, especially in a world of usage-based pricing, staggered collections, and multi-system data fragmentation. Mid-cycle credit notes and refunds can wreak havoc on revenue integrity. And in most organizations, accountants are still manually patching over these timing mismatches with spreadsheets and detective work, rather than true automation.

The reality? Most finance teams know they need accuracy, but they’re searching online for ways to:

- Handle refunds without introducing general ledger inconsistencies

- Automate journal entries without relying entirely on ERP customization

- Build stopgap solutions in Excel to bridge operational gaps

In this guide, we break down how modern finance teams are rethinking adjusting entries—from Excel workarounds to system-wide automation.

Why do you need to adjust entries?

Think of them as clean-up entries before you finalize the books. They help:

Common scenarios where adjusting entries are required

Adjusting entries are made at the end of an accounting period — before financial statements are finalized.

They ensure that all revenues earned and expenses incurred during the period are reflected, even if the cash hasn’t moved yet.

In some cases, mid-cycle adjustments are also needed — especially when there are events like refunds, credit notes, or contract changes that materially impact revenue recognition system.

How to adjust entries when refunds and credit notes flow mid-cycle?

Step 1: Identify accounts needing adjustment

Inputs: Refund notifications, credit note logs, ERP reports, gateway exports.

Real-life tip: Many refunds never reach accounting unless support notifies you. Bridge this gap with a shared refund tracker (like a Google Sheet or shared Excel file) to ensure refunds/credit notes are logged in real-time. This can be updated by both support and finance teams, preventing missed adjustments.

Example chart: Refund recon discrepancy

This chart is used by revenue accountants and support teams for tracking individual customer refunds monthly and ensuring that every refund has been accurately processed.

It is used during the reconciliation process, when refund transactions are logged and discrepancies are identified and resolved.

How to build a shared refund tracker manually

🧩Use Excel/Google Sheets with:

- Data validation dropdowns for refund status

- Conditional formatting for missing GL entries

- Filters/pivot tables for monthly summaries

However, the shared refund tracker presents some glaring challenges:

- Manual updates: Both the finance and support team must manually input data, which increases the risk of human error, especially when the volume of refunds and credit notes grows.

- Data reconciliation: Refund amounts recorded in the payment gateway (Stripe, PayPal, etc.) might not always match the amounts recorded in the ERP or accounting system due to system configurations, currency differences, or accounting periods.

- Timing discrepancies: Refunds and payments might not be processed or recorded at the same time, especially if there are delays in the payment gateway or ERP system updates. The timing difference can cause discrepancies between the data.

- Lack of transparency: Different teams (Finance, Operations, Support) might not have access to the same data, which can lead to discrepancies in understanding why certain refunds were processed differently. Without visibility into the processes, it becomes difficult to reconcile figures across departments. Refunds and credits may not always be categorized properly in the chart too, leading to confusion when trying to track the discrepancies.

- Scalability: As the company scales, the sheer volume of transactions can become overwhelming to manage in a shared spreadsheet. It might lead to version control issues (who's editing what), difficulty in handling large amounts of data, and potential delays in reconciling.

- Audit trail: If a refund wasn’t logged properly, it could create an issue during an external audit. The auditor might flag discrepancies, leading to delays and additional work as it may be hard to trace the origin of the errors.

- Complexity of refund policies: Refund policies and procedures can vary significantly across products, regions, and sales channels, adding complexity to the tracking and reconciliation process.

Step 2: Review trial balance and look for discrepancies

What to look for:

- Negative accounts receivable balances

- Unexpected dips in revenue

- Customer balance mismatches between ERP and gateway

Example chart: Refund recon discrepancy

This chart is used by CFOs at a higher level to provide a monthly summary of refund discrepancies to evaluate overall performance and discrepancies at the company-wide level rather than looking at individual transactions.

It is used in monthly financial reviews or management reporting, offering an aggregate view of discrepancies and their impact on revenue.

Action: Investigate $7K difference by reviewing specific transactions.

Step 3: Apply the Matching Principle

Revenue previously recognized must now be reversed in the same period as the service impact.

Scenario: $1,200 SaaS subscription billed and recognized upfront on Jan 1. Customer churns on Jan 15. Refund of $600 issued.

Entry:

- Dr. Revenue $600

- Cr. Accounts Payable / Cash $600

Matching COGS (cost of goods sold) to the correct revenue period gives a more accurate picture of profitability for that period. This ensures that the company's financial statements reflect the true financial performance during each period, rather than skewing the results based on the timing of cash receipts or payments.

Step 4: Calculate the adjustment amount

Use proportion-based formulas or direct billing values.

Proportion-based formulas: This involves using a percentage or proportion of the total amount to calculate specific values. For example, if you're calculating a refund for a customer who paid upfront for a subscription, you might determine how much of the refund corresponds to the portion of the service that was delivered up to that point. If the service lasts for 12 months, and the customer is entitled to a refund for 3 months, you'd use a proportion-based formula to calculate the refund (i.e., 3 months out of 12 months).

🧠Manual calculation of refunds using proportions is complex and prone to errors, especially when dealing with multiple customers, varying service periods, or different pricing structures.

Direct billing values: This refers to using actual figures from billing records (such as invoices or payments) to determine the necessary adjustments or entries. For example, if you need to account for a credit note, you would simply refer to the specific amount on the credit note and use that exact figure when adjusting the accounting entries.

🧠Manually cross-referencing billing records, invoices, and credit notes introduces the risk of overlooking discrepancies or entering incorrect data into the general ledger.

Formula: Refund = (Unused Period / Total Period) * Total Invoice Amount

Example:

- Subscription = $1,200/year

- Churn at 6 months

- Refund = (6/12) * $1,200 = $600

Step 5: Prepare and post adjusting entry

Debit and credit the appropriate accounts.

Use a contra revenue account if you want to track reversals separately.

Wait, what’s a contra revenue account?

A contra revenue account is a specialized account in the general ledger that is used to track reductions in revenue, such as refunds, discounts, or credit notes.

It essentially allows businesses to record these reductions separately from the primary revenue account while still impacting the overall financial performance.

Revenue accountants are typically responsible for maintaining contra revenue accounts. These teams monitor and update the account whenever a revenue adjustment (e.g., a refund or credit note) is recorded.

CFOs, senior revenue accountants, and controllers oversee the contra revenue accounts to ensure that all adjustments are accurately recorded and accounted for. The CFO is often responsible for the final financial statements, while the revenue accountant will manage the day-to-day adjustments and ensure they are in compliance with accounting policies.

How to track revenue reversal:

Here’s how the contra revenue account might work in practice:

In this example:

- The Sales Revenue account is credited with $10,000 for the total sale.

- The Contra Revenue - Refunds account is credited with $1,000 to track the refunds issued to customers.

- The Net Revenue of $9,000 is reported on the financial statements, reflecting the true revenue after refunds.

Warning: Reconciling the contra revenue account with other financial accounts (like accounts receivable, revenue, or refunds) can be cumbersome. Differences between these accounts may arise, especially if adjustments are not recorded promptly or consistently.

Best practices for revenue accountants for adjusting entries

- Reconcile bank, ERP, and payment apps regularly instead of waiting for month-end.

- Standardize classification of expenses to avoid misclassification.

- Maintain audit logs to have clean audit trails.

- Automate wherever possible by:

- Integrating operational data from various systems (ERPs, payment gateways, CRM)

- Automatically posting journal entries in real time, based on defined revenue schedules

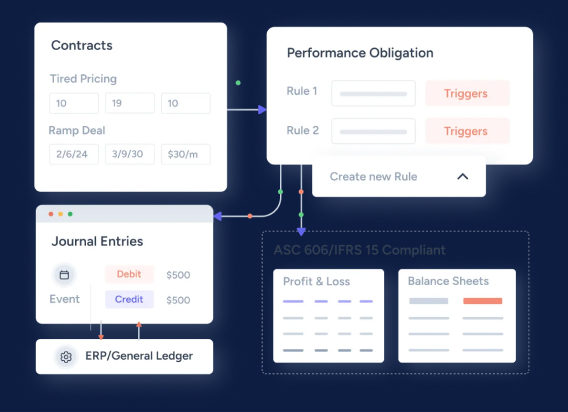

How Zenskar adjusts journal entries automatically

Zenskar automatically identifies the accounts needing adjustments based on predefined rules for refunds, revenues, and expenses. Here’s a teardown of the steps involved that require no manual oversight:

Ingestion of data

Zenskar automatically ingests relevant financial data from ERP systems (e.g., invoices, payments, contracts) and payment gateways. It ensures that all billing activities related to revenue are captured and accounted for.

Usage data tracking

Zenskar tracks service usage and ensures that revenue is recognized only when earned. It also links consumption data with invoicing, automatically generating journal entries based on service usage.

Invoicing

Once revenue tracking is complete, invoices are generated. Zenskar automates this process for customers based on usage or contract terms, ensuring that revenue is recognized and reflected in the general ledger in real time.

Journal entry creation

After the necessary data is gathered and invoicing is complete, Zenskar automatically creates journal entries, adjusting for accrued or deferred revenue. Zenskar creates and posts journal entries based on invoicing data and the company’s revenue recognition rules. This reduces manual data entry and ensures consistent and accurate posting in the general ledger.

Reconciliation

Once journal entries are created, the reconciliation process begins. Zenskar automatically reconciles payment data from gateways and bank accounts with the journal entries. This ensures that the payments and journal entries are in sync and any discrepancies are resolved without manual intervention.

In summary, Zenskar’s automation of the adjusting entries process offers a unified, scalable solution that addresses the pain points of accuracy, efficiency, and real-time financial visibility, making it the go-to platform for revenue automation. It captures financial data from ERPs and payment gateways, tracks usage, generates invoices, and creates journal entries based on predefined revenue recognition rules. The system also automatically reconciles payments, ensuring accuracy and reducing manual effort.

Zenskar eliminates the manual workload, allowing accountants and CFOs to focus on higher-value tasks. Take an interactive tour to see us in action, or book a free demo (no strings attached) to evaluate if we are the right fit for your organization.

Frequently asked questions

Adjusting entries are journal entries used to recognize revenues and expenses in the proper period to ensure that a company's financial statements accurately reflect its financial position.

To record a refund, reverse the recognized revenue by debiting the revenue account and crediting accounts payable or cash, depending on how the refund is processed.

Yes, adjusting entries can be automated using revenue automation systems like Zenskar, which automatically track usage, generate invoices, create journal entries, and reconcile discrepancies without manual intervention.

Adjusting entries align revenue and expenses with the correct accounting period, while correcting entries fix errors in previously recorded transactions.

Adjusting entries are required when there are timing mismatches between when revenue or expenses are recognized and when cash is exchanged, such as unbilled revenue, accrued expenses, or refunds issued after revenue recognition.